Significant developments have marked the mortgage lending landscape in the first quarter of 2025. According to Gallagher Re’s Mortgage Market Report for Q1 2025, Gross Domestic Product (GDP) expanded by 0.7% during the quarter and 2.7% annually, indicating continued economic strength.

The unemployment rate remained steady at 4.1%, while personal income per capita reached an all-time high of $73,400 per household. Despite these positive economic indicators, mortgage rates have edged back toward 7%, influenced by tempered expectations for Federal Reserve interest rate cuts. Home prices continued to rise, with a 4.0% year-over-year increase, reaching new highs.

The mortgage lending industry constantly evolves, influenced by interest rate fluctuations, economic conditions, housing market trends, and regulatory shifts. The first quarter of 2025 has brought significant developments that impact lenders, borrowers, and investors. This in-depth Q1 2025 Mortgage Lending Report provides a comprehensive analysis of mortgage lending trends, key challenges, and the future outlook for the industry.

Table of Contents

Economic Overview and Market Conditions

The U.S. economy entered 2025 with cautious optimism. Inflation, a persistent concern throughout 2024, showed signs of easing, allowing the Federal Reserve to adjust its monetary policy accordingly. In Q1 2025, the Fed reduced interest rates by 50 basis points to stimulate economic growth and improve affordability in the housing sector. This move led to declining mortgage rates, making homeownership slightly more accessible for many Americans.

However, economic uncertainty and affordability concerns continue to shape borrower behaviour. While job growth remained stable, wage growth did not keep pace with housing price appreciation. As a result, demand for mortgage loans was uneven, with some borrowers taking advantage of lower interest rates while others remained hesitant due to high home prices and economic unpredictability.

Mortgage Lending Trends in Q1 2025

Decline in Mortgage Origination Volume

Mortgage origination volumes declined in Q1 2025 compared to the previous year. According to industry data, total mortgage origination dropped by approximately 6.7%, marking the lowest since 2000. Several factors contributed to this decline, including tight housing inventories, high property prices, and stringent lending criteria implemented by financial institutions.

While refinancing activity saw a modest uptick due to lower interest rates, purchase mortgage applications remained subdued. Many prospective homebuyers faced affordability challenges, especially first-time buyers struggling to meet down payment requirements and qualify for loans under the new regulatory environment.

Increase in Non-Traditional and Alternative Lending

With traditional mortgage products becoming less accessible to specific borrowers, non-traditional lending gained momentum in Q1 2025. Non-QM (Non-Qualified Mortgage) loans, which cater to self-employed individuals and those with unconventional income sources, saw increased demand.

Lenders also expanded offerings in alternative mortgage products, such as interest-only loans and adjustable-rate mortgages (ARMs), which provided borrowers with more flexible financing options. These products, however, come with risks, significantly if interest rates fluctuate in the future.

Growth of Technology-Driven Mortgage Solutions

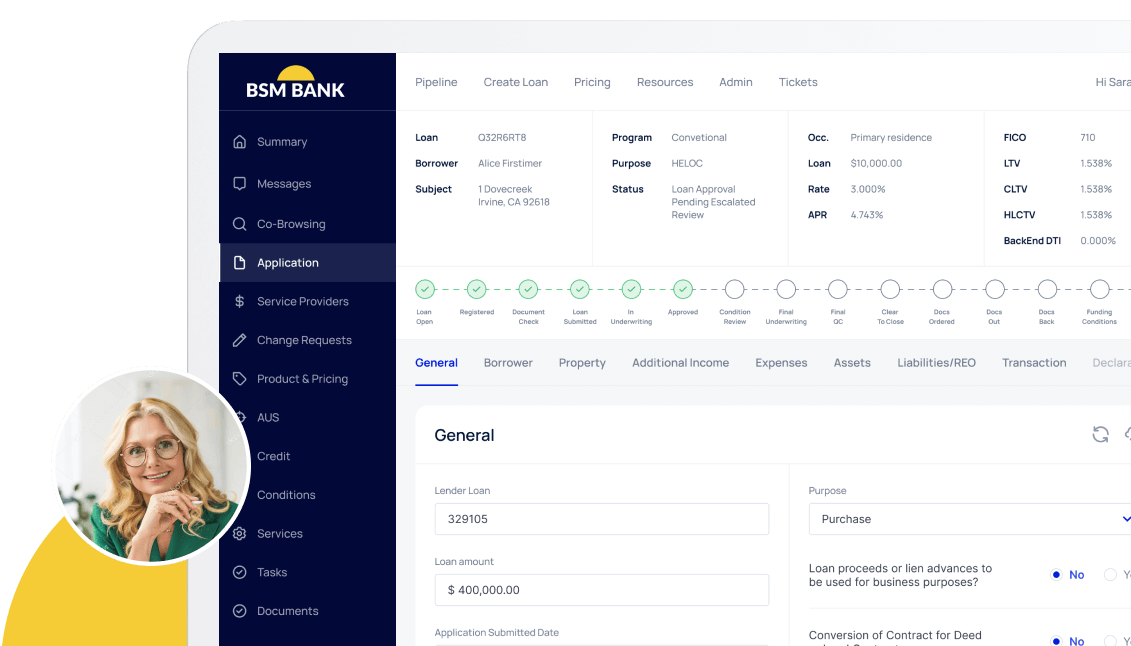

The mortgage lending landscape has continued its digital transformation. More lenders are leveraging technology to streamline application processes, improve customer experiences, and enhance underwriting accuracy. Automated underwriting systems, artificial intelligence (AI)-powered risk assessments, and blockchain-based mortgage transactions gained traction in Q1 2025.

The adoption of mortgages and digital closings also increased, reducing paperwork and expediting the loan approval process. Mortgage lenders that have embraced digital transformation are seeing higher efficiency and customer satisfaction rates.

United States Market Insights

The U.S. housing market remained highly competitive, stabilizing home prices but still significantly higher than pre-pandemic levels. Major metropolitan areas continued to experience strong demand, although affordability remained a critical issue. The Sun Belt states, including Florida, Texas, and Arizona, saw increased migration and home sales activity, while Northeast and West Coast markets faced affordability-driven slowdowns.

Policy Developments and Their Impact on Mortgage Lending

Regulatory Changes and Mortgage Qualification Standards

Government policies and regulatory changes played a significant role in shaping mortgage lending in Q1 2025. New lending regulations to prevent excessive risk-taking required lenders to adopt more rigorous qualification criteria.

Subscribe to BeSmartee 's Digital Mortgage Blog to receive:

- Mortgage Industry Insights

- Security & Compliance Updates

- Q&A's Featuring Mortgage & Technology Experts

In the U.S., the Consumer Financial Protection Bureau (CFPB) introduced updated affordability assessments to ensure borrowers do not take on unmanageable debt. These measures impacted approval rates, particularly for lower-income applicants.

Government-Sponsored Housing Programs

To boost homeownership, several government-backed programs were expanded in Q1 2025. The Federal Housing Administration (FHA) increased loan limits in high-cost areas, while Fannie Mae and Freddie Mac introduced new loan products with lower down payment requirements.

In addition, first-time homebuyer assistance programs received additional funding, providing grants and interest-free loans to eligible buyers. These initiatives were designed to make homeownership more attainable amid rising property prices.

Challenges Facing Mortgage Lenders

Affordability and Housing Inventory Constraints

Despite lower mortgage rates, affordability remains a significant challenge. The supply of affordable homes has not kept pace with demand, leading to bidding wars and rising home prices. Many buyers, especially millennials and Gen Z, find it increasingly difficult to enter the housing market.

Credit Tightening and Risk Management

Lenders have tightened credit standards due to economic uncertainty and regulatory pressures. Borrowers with lower credit scores or irregular income streams faced difficulties obtaining mortgage approvals. Risk management strategies became more stringent, with lenders focusing on ensuring long-term borrower stability.

Rising Delinquency Rates

Early indicators suggest a slight increase in mortgage delinquencies in Q1 2025, particularly among borrowers who took out loans during the higher interest rate period of 2023-2024. While delinquency rates remain relatively low compared to historical averages, lenders monitor this trend closely to assess potential risks.

Future Outlook for Mortgage Lending

The outlook for mortgage lending in the remainder of 2025 has become more uncertain due to recent economic developments. In January, the Consumer Price Index (CPI) rose by 0.5% month-over-month, surpassing expectations and bringing the annual inflation rate to 3.0%.

This uptick in inflation has diminished the likelihood of imminent interest rate cuts by the Federal Reserve. According to Reuters, Dallas Federal Reserve Bank President Lorie Logan emphasized the need for caution regarding potential rate reductions, even if inflation approaches the 2% target.

However, affordability issues and inventory shortages will continue to challenge homebuyers. Lenders must adopt innovative strategies to address these issues, including offering flexible loan products, expanding digital mortgage services, and participating in government-backed housing programs.

Roundup

Q1 2025 has been a pivotal period for mortgage lending, characterized by economic shifts, policy changes, and evolving borrower behaviours. While lower interest rates have provided some relief, affordability and lending constraints remain central challenges. Lenders, borrowers, and policymakers must work together to create a sustainable and inclusive mortgage market.

Navigating the mortgage landscape requires expertise, technology, and a customer-centric approach. At BeSmartee, we empower lenders with innovative digital mortgage solutions that streamline processes, enhance efficiency, and improve borrower experiences. Contact us today to learn how we can transform your mortgage originations.